Corporate Finance

Most growing companies raise money more than once: a bank line, then a mezzanine layer, then an equity round when the balance sheet can’t stretch further. We’ve structured debt and equity for Pacific Northwest companies for six decades, and we draft each financing so the next raise isn’t fighting the last one.

Talk to an attorneyFounded

1965

Attorneys

11

AV-rated

Martindale-Hubbell

Office

Bellevue, WA

Founded

1965

Attorneys

11

AV-rated

Martindale-Hubbell

Office

Bellevue, WA

Corporate finance attorneys for Bellevue and Seattle companies

Oseran Hahn structures the capital growing companies raise: bank lines and term loans, mezzanine layers, equity rounds, and the shareholder loans that sit somewhere in between. We review the term sheet and personal guaranty before you sign, negotiate the covenants and security terms, and flag the obligations that follow the company long after the money lands. Most companies raise more than once, and a clean financing makes the next one easier to close.

How a company raises money shapes who it answers to afterward, so the instrument matters as much as the amount. We weigh debt against equity and structure the raise around it; paper the senior bank and SBA debt that comes cheapest; handle the equity and convertible instruments that bring capital without a repayment schedule; layer in the mezzanine and subordinated debt that bridges the two; and negotiate the covenants and closing terms that govern the financing for as long as it's outstanding.

Debt vs. equity: structuring the raise

The first question in any financing is what kind of capital the company is taking on, because debt and equity behave nothing alike after the money lands. Debt is cheaper and doesn’t dilute ownership, but it has to be repaid on a schedule regardless of how the business performs, and lenders secure it against the company’s assets. Equity never has to be repaid, but it gives away a piece of the company and, often, a vote on major decisions. Most growing companies use both, layered into a capital stack, and the order matters: senior debt sits first in line for repayment, equity sits last.

How a shareholder’s contribution is characterized carries tax consequences that surprise owners. Money an owner puts in as debt generates deductible interest and a clean repayment path; the same money as equity does neither, and the IRS can recharacterize a purported loan as equity under IRC § 385 if it isn’t documented and serviced like real debt. Interest deductibility itself is capped for larger companies under IRC § 163(j). We structure the raise, and document the instruments, so the tax treatment matches the intent rather than working against it.

Senior bank and SBA debt

Senior secured debt is the cheapest capital most closely-held companies can get, and it arrives with the most paper. A term loan or revolving line of credit comes with a loan agreement, a promissory note, a security agreement, and almost always a personal guaranty from the owner. The lender perfects its security interest by filing a UCC-1 financing statement under Article 9 of Washington’s Uniform Commercial Code (RCW 62A.9A), which fixes its priority against later creditors. We review the collateral description, the guaranty scope, and the financial covenants before the owner signs, because the default provisions and the guaranty are where a routine loan turns into a personal-liability problem.

SBA-backed financing, the 7(a) and 504 programs, extends terms and lowers the down-payment requirement for businesses that don’t fit conventional underwriting, at the cost of a longer approval timeline and more documentation. We handle the loan-document review, negotiate the covenants and guaranty terms that are actually negotiable, and flag the ones that aren’t, so the owner knows exactly what’s pledged and what triggers a default before closing.

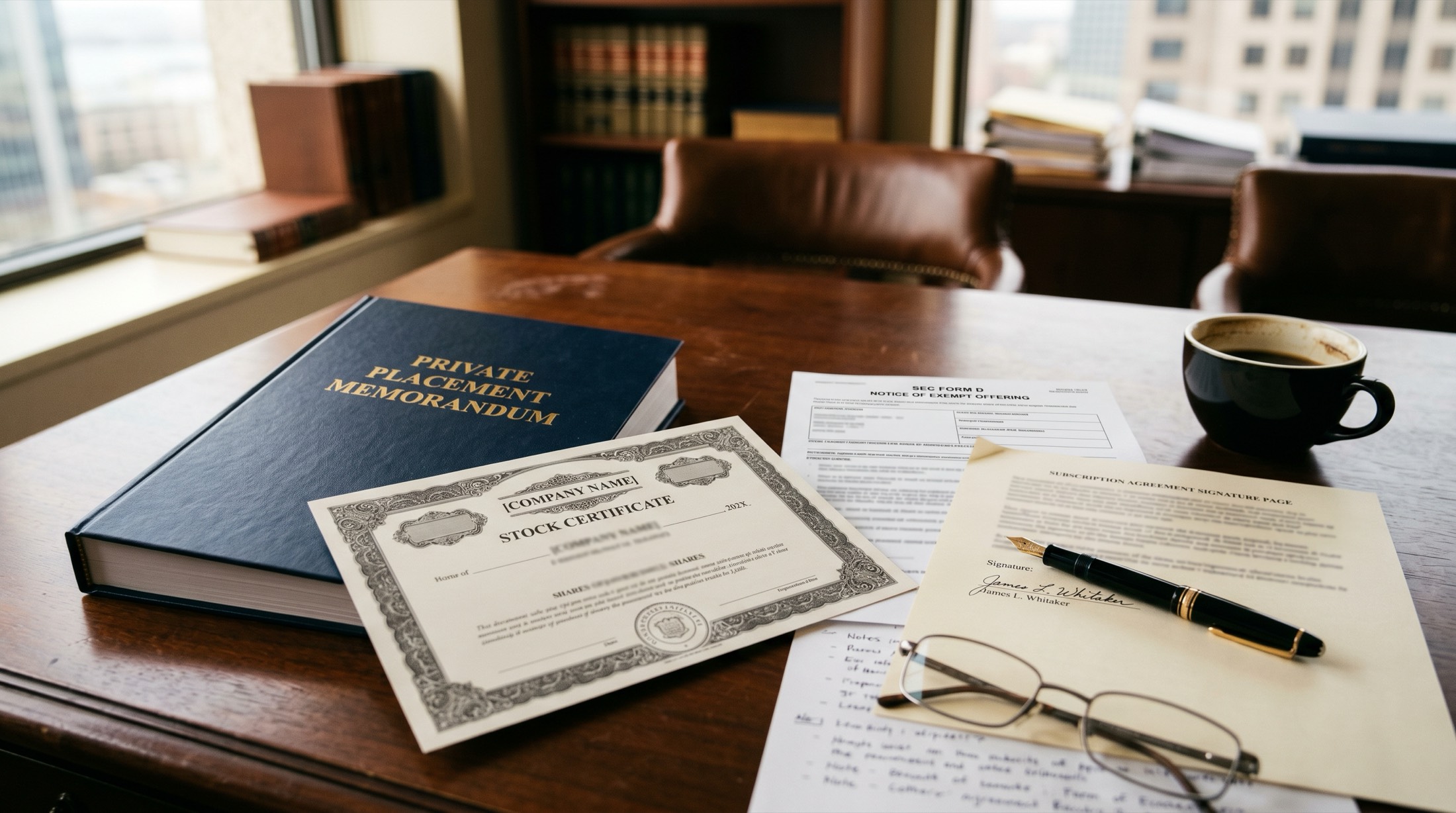

Equity and convertible financing

Raising equity means selling a security, and securities law applies whether the company is a startup or a fifty-year-old manufacturer. Most private raises rely on the safe harbors in SEC Regulation D under the statutory private-placement exemption of Securities Act § 4(a)(2) (15 U.S.C. § 77d(a)(2)): Rule 506(b) permits an unlimited raise from accredited investors and up to 35 sophisticated others without general solicitation, while Rule 506(c) allows public solicitation but requires verifying that every investor is accredited under Rule 501. Both require a Form D filing within fifteen days of the first sale, and Washington’s blue-sky requirements under the Securities Act of Washington (RCW 21.20) apply on top. Get the exemption wrong and investors can have a rescission right, which is the last thing a company wants hanging over its cap table.

Early-stage companies often raise on convertible instruments, SAFEs or convertible notes, that postpone the valuation fight to a later priced round. For raises that need to reach beyond accredited investors, Regulation Crowdfunding and Regulation A offer registered alternatives with their own disclosure burdens. We draft and review the priced-round documents, the stock purchase agreement, investor rights, voting and co-sale agreements, alongside the convertible instruments, with attention to how conversion mechanics, valuation caps, and liquidation preferences interact with the founders’ existing equity. For C-corporations, we structure the raise to preserve Qualified Small Business Stock eligibility under IRC § 1202 where the founders qualify.

Mezzanine and subordinated debt

Between senior debt and equity sits a layer of financing that does some of the work of both. Mezzanine and subordinated debt carry higher interest rates than bank loans and usually come with warrants or a conversion feature that gives the lender an equity upside, but they sit behind the senior lender in priority and ahead of the equity holders. Growing companies reach for this layer when the senior lender won’t extend more and the owner doesn’t want to dilute further at the current valuation.

The defining document of a multi-lender capital structure is the intercreditor or subordination agreement, which spells out who gets paid first, who can exercise remedies on a default, and what the junior lender can and can’t do while the senior debt is outstanding. These agreements are heavily negotiated and easy to get wrong; a subordination provision broader than the owner realized can freeze the junior lender out entirely in a workout. We draft and negotiate the intercreditor terms with the whole capital stack in view, not just the instrument in front of us.

Closing, covenants, and the life of the financing

A financing doesn’t end at closing; the covenants govern the company for as long as the money is outstanding. Affirmative covenants require the company to do things, deliver financial statements, maintain insurance, keep collateral in good standing. Negative covenants restrict what it can do without the lender’s consent, take on more debt, pay dividends, sell assets, change ownership. Financial covenants, a minimum debt-service-coverage ratio or a maximum leverage ratio, get tested every quarter, and a company that trips one is technically in default even when every payment is current. We negotiate covenant headroom at the front end and help clients manage compliance after the money lands.

When a covenant is breached or a payment is missed, the path runs through a waiver, an amendment, or a workout before it reaches enforcement. We’ve sat on both sides of that conversation, and the relationship with the regional lender often matters as much as the document. A clean amendment negotiated early beats a default notice answered late. The same care that goes into the original financing goes into keeping it healthy.

Six decades of corporate finance work means we’ve represented the company taking the money and, in other matters, the lender and investor putting it in. We know which terms are market, which are negotiable, and which ones the owner will regret. That perspective shapes every financing we paper.

Debt, equity, and tax under one roof.

A capital raise crosses lending law, securities law, and tax all at once. The tax group sits next to the finance practice, so the instrument gets structured for the after-tax result, not just the closing.

The whole capital stack in view.

We draft the senior loan knowing the mezzanine layer is coming and the equity round after that. Financing structured one layer at a time is how owners end up with covenants that fight each other. We draft for the stack.

Same partner from term sheet to workout.

The partner who negotiates the loan agreement is the same one who handles the amendment when a covenant gets tight two years later. The relationships with regional lenders carry across the life of the financing.

The attorneys behindthe work.

Our business and corporate attorneys handle this work alongside our litigation team, so you have coverage whether your matter stays transactional or becomes something more.

What clientsask us first.

How long does a financing take to close?

A conventional bank loan with clean collateral can close in three to six weeks; an SBA-backed loan runs longer because of the approval process. A priced equity round typically takes one to three months from term sheet to closing. The diligence and the lender’s or investor’s process, not the drafting, usually set the pace.

Do you handle both debt and equity financings?

Yes. We structure senior bank and SBA debt, mezzanine and subordinated debt, convertible instruments, and priced equity rounds, plus the recapitalizations that combine them. Most growing companies use more than one over their life, and we draft each with the others in mind.

Do you represent the company, or the lenders and investors?

On any given financing we represent one side, usually the company raising the capital, and we say so in the engagement letter. We’ve sat on the lender and investor side in other matters, which is what tells us where a term sheet is genuinely market and where it’s just aggressive.

Do you work with out-of-state lenders, investors, and SBA lenders?

Yes. We coordinate with regional and national banks, SBA lenders, private credit funds, and out-of-state investors and their counsel, and we handle the Washington securities filings and UCC perfection directly so the financing closes on schedule.

What happens if the company trips a covenant or can’t make a payment?

That’s a workout, and how it’s handled early decides how it ends. We negotiate waivers and amendments with the lender before a default notice lands, and our litigation and creditor-debtor team is in the same office if enforcement becomes a real risk. We draft knowing what gets tested.

When is it time to bring in corporate finance counsel?

When the bank has sent a term sheet and a personal guaranty. When you’re taking on outside equity and the investor’s lawyer drafted the documents. When growth has outrun the line of credit and you need a mezzanine layer. Or when a shareholder wants to put money in and you’re not sure whether it’s a loan or equity. The terms you sign now set what the next round has to live with, so it’s worth structuring early.

Recentarticles.

Same-day call. Confidential intake. No engagement until both sides decide it fits.

Oseran Hahn P.S. · 11225 SE 6th St, Suite 100 · Bellevue, WA 98004

This content is provided for general informational purposes only and does not constitute legal advice. Viewing this page does not create an attorney-client relationship.